YouTube TV's Genre Plans Reshape Marketing Reach

YouTube TV's February 2026 shift to genre-specific plans fragments its subscriber base into self-selected audience segments that create stronger targeting signals and reduce ad waste. This article explains how advertisers must adjust their CTV reach planning, targeting strategy, and budget allocation to take advantage — or risk losing efficiency as subscriber migration causes frequency gaps.

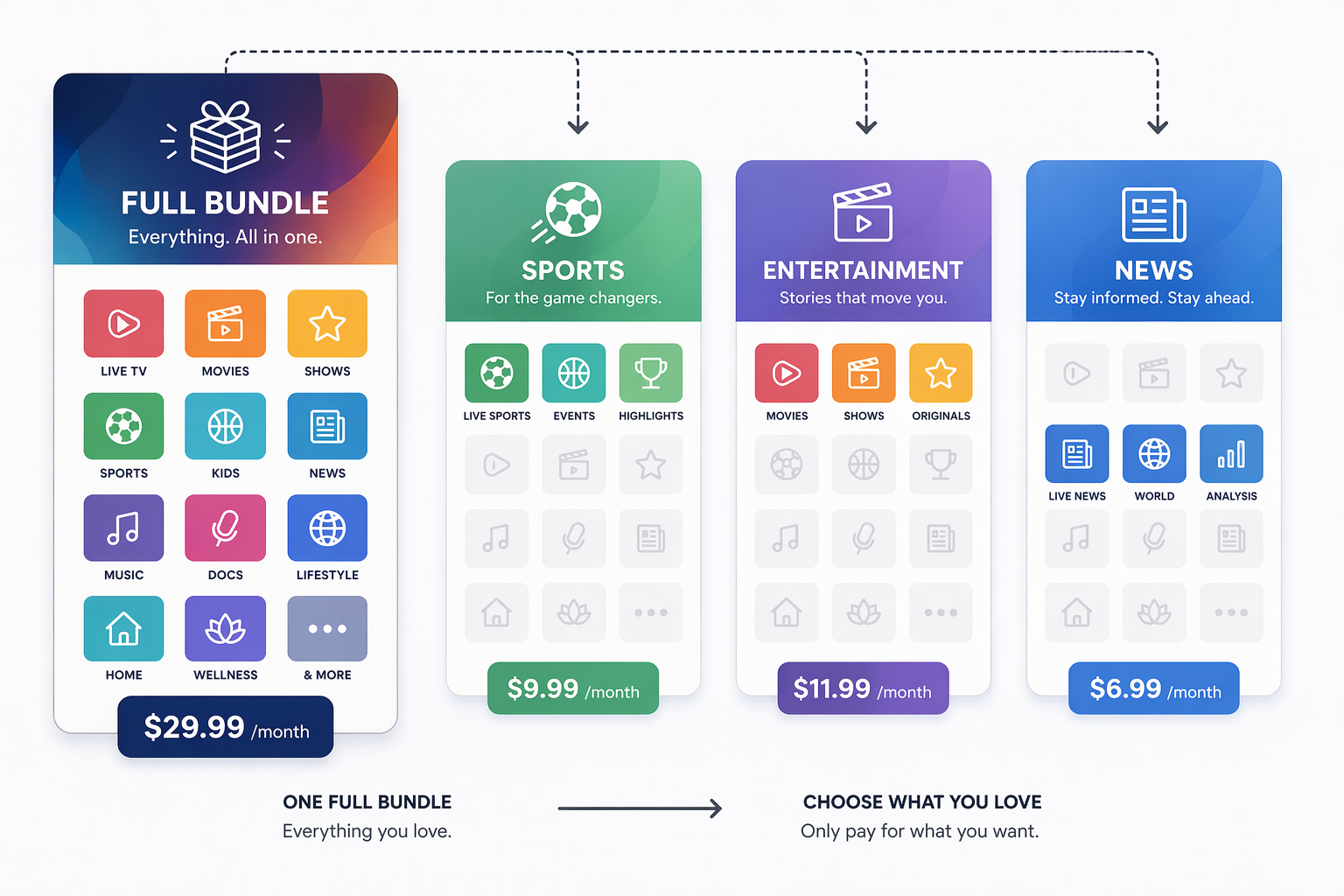

YouTube TV's genre plans turn a familiar CTV planning shortcut into a liability. Before the February 2026 restructure, a buyer could treat the $82.99 full bundle as the practical default: one large subscriber pool, one broad channel universe, one reach assumption to pressure-test. Now the same platform is asking subscribers to sort themselves into cheaper genre packages, and that sorting matters more to advertisers than the monthly price does.

The important shift is not that YouTube TV added discount tiers. It is that the Sports Plan, at $64.99 per month, is $18 cheaper than the full Base Plan while excluding whole categories of entertainment and news channels. The Entertainment Plan is $54.99, the News Plan is $44.99, and additional niche options include Family, Kids & Family, and Spanish-Language plans.[1] That is not just packaging. It is subscriber-declared intent.

The New Planning Unit Is The Genre Plan

The channel mix is where the advertising implication starts. A sports subscriber is not merely reachable in sports content; that household has accepted a narrower TV bundle to keep ESPN, FS1, NFL Network, and MLB Network. An entertainment subscriber has made a different trade-off around networks such as AMC, Bravo, Discovery, E!, Food Network, HGTV, and TLC. A news subscriber has opted into a package centered on CNN, Fox News, MSNBC, and CNBC.[1]

| Plan | Announced Monthly Price | Core Channel Signal | Planning Implication |

|---|---|---|---|

| Base Plan | $82.99 | Full channel lineup | Still the cleanest starting point for broad reach assumptions. |

| Sports Plan | $64.99 | ESPN, FS1, NFL Network, MLB Network | A stronger sports-affinity signal, but narrower non-sports exposure. |

| Entertainment Plan | $54.99 | AMC, Bravo, Discovery, E!, Food Network, HGTV, TLC | Useful for lifestyle and entertainment context, weaker for sports/news reach. |

| News Plan | $44.99 | CNN, Fox News, MSNBC, CNBC | More explicit news-context selection, with reduced entertainment and sports coverage. |

| Niche Plans | Varies by tier | Family, Kids & Family, Spanish-Language and related packages | Potentially useful for contextual fit, but not a substitute for total-platform reach. |

YouTube's own announcement framed the move as a way to give viewers more choice and lower-cost options starting in early 2026.[2] For media teams, the operational question is sharper: when subscribers choose a genre package, how much of yesterday's YouTube TV reach model still holds?

Self-Selection Improves The Signal, Then Shrinks The Assumption

Genre plans create a cleaner first-party-style context signal than many inferred audience segments. A household that pays for the Sports Plan is making a more visible choice than a household placed into a sports-interest segment because someone watched a highlight clip or visited a team page. The value is practical: less budget leaks into viewers who happen to be in a broad CTV pool but are unlikely to care about the sports context.

That same choice narrows the pool. YouTube TV's scale is meaningful, but it is not all of YouTube. Tatari cites about 9.4 million YouTube TV subscribers, while other market estimates sit in a wider 9 million to 12 million range.[3] For planning purposes, the conservative read is that YouTube TV is a large bounded subscriber product inside a much larger YouTube viewing ecosystem.

The distinction matters because YouTube overall has become central to television-screen behavior. Nielsen data cited in 2025 showed YouTube as the most-watched service on U.S. televisions at roughly 11.6% to 12.4% of total TV viewing time, ahead of Netflix, while streaming overall reached 44.8% of TV usage.[4] That explains why advertisers care. It does not mean every YouTube TV genre tier should be modeled as if it carries YouTube's full TV-screen dominance.

Where The Old Reach Curve Breaks

The old single-pool assumption breaks in three places: composition, duplication, and frequency. None of those changes is dramatic on its own. Together, they can turn a clean-looking CTV plan into uneven delivery.

Composition Drift

Composition drift is the first maintenance problem. If budget was planned against a blended YouTube TV audience, and a meaningful share of sports-motivated households migrates into the Sports Plan, the remaining full-bundle audience may no longer carry the same genre balance. The platform name stays the same; the audience mix underneath it moves.

For a beer, auto, sportsbook, QSR, or athletic apparel advertiser, that movement may be useful. A sports-heavy plan can reduce wasted impressions against households that were only present because the old bundle forced sports, entertainment, and news into one package. For a broad consumer brand that bought YouTube TV for national reach across household types, the same migration can create missing exposure if the plan does not explicitly account for where entertainment and news viewers went.

Frequency Gaps

Frequency is the quieter issue. A campaign that caps frequency across a broad YouTube TV buy may look controlled in the aggregate while over-serving one plan and under-serving another. If sports inventory absorbs a disproportionate share of spend because it is easier to justify contextually, entertainment and news subscribers may receive too few exposures to move brand metrics. If the buy is split too mechanically across plans, the reverse can happen: budgets spread thinly enough that no segment reaches effective frequency.

This is not a call to invent precision where the platform does not provide it. It is a call to stop reading average frequency as if all YouTube TV impressions now come from the same audience behavior. A post-fragmentation plan needs to show frequency by relevant genre inventory, not only by total platform delivery.

Duplicated Reach

Duplication also becomes harder to hand-wave. A household may remain in the Base Plan, move into a genre plan, or be reached elsewhere across YouTube's broader CTV environment. Without plan-aware reporting, a campaign can count incremental-looking inventory that is really just repeated exposure against the easiest-to-buy segment.

That is especially important for Q3 and Q4 2026 planning because seasonal sports demand can pull money toward the Sports Plan before teams have enough evidence that the added impressions are incremental to the rest of the video plan. The Sports Plan is a useful signal. It is not, by itself, proof of incremental reach.

How To Allocate Budget After The Split

Budget allocation should start with the campaign's job, not with the novelty of the package. The same genre split can be efficient or wasteful depending on whether the advertiser is buying context, reach, or proof of attention.

- Isolate sports inventory when the brand has a real reason to pay for sports attention: game-adjacent launches, fandom-driven creative, sponsorship amplification, local dealer pushes around sports seasons, or categories where sports viewing is part of the purchase context.

- Mix genre plans when the audience is broad but the creative changes by context, such as a retailer using different messages for family, entertainment, and news environments.

- Keep Base Plan or cross-plan coverage when the objective is national reach, household penetration, or upper-funnel awareness that should not depend on one content affinity.

- Use niche tiers only when the audience or language context is central to the brief; do not treat smaller contextual tiers as cheap substitutes for platform-level scale.

CPM discipline matters here. Digital Applied reports a $24 to $32 CPM range for connected TV inventory, and AI Digital also frames YouTube TV as premium CTV inventory; sports can command a premium within that environment.[5][6] That range should not be treated as a fixed YouTube TV rate card. Seasonality, targeting, demand, and plan tier can all move actual pricing.

At the high end of the market, the buy has to be justified as attention and reach, not as cheap response media. Digital Applied reports 84%+ ad completion on connected TV compared with 62% on mobile, which supports the case for lean-back attention quality.[5] It does not turn YouTube TV into a click channel. The right measurement frame is reach, frequency, completed views, brand lift, incrementality, and downstream modeled contribution, not click-through rate.

For teams building broader CTV measurement systems, this is where incrementality design matters more than another dashboard view. Internal planning resources such as an AI-powered CTV advertising guide can help connect plan-level delivery to brand and business outcomes without pretending that a living-room ad should behave like a paid search click.

Sports Planning Needs A Timing Caveat

The Sports Plan will get the most attention because the audience signal is obvious and because live sports already carry scarcity value in CTV. But Q3-Q4 2026 plans need to separate current inventory from announced future inventory.

Variety reported that ESPN Unlimited integration is expected in fall 2026 and will add ESPN+ content to the Sports Plan.[1] Until that inventory is actually available and buyable, it should not be counted in summer reach forecasts, guaranteed impression plans, or pre-fall frequency models.

That caveat is not a reason to avoid the Sports Plan. It is a reason to keep two versions of the sports reach model: one for current Sports Plan inventory, and one scenario that includes ESPN Unlimited only after the launch terms, inventory access, and reporting treatment are clear.

Access Still Filters Who Can Act On The Signal

The genre signal is only useful if the buyer can actually access the inventory. YouTube TV inventory is bought through Display & Video 360 rather than standard Google Ads workflows, which creates a practical barrier for smaller advertisers or teams without DV360 seats, partners, or managed-service access.[6]

That access constraint changes the recommendation. A large agency team can treat genre plans as a CTV planning lever inside a broader programmatic video strategy. A smaller advertiser may need to work through a partner, compare DSP access, or decide that broader YouTube CTV placements are more realistic than direct YouTube TV inventory. For buying mechanics, the useful companion reads are the guide to YouTube TV inventory pools and the DSP comparison guide.

This is also why agency adoption matters. Business Insider, citing a Pixability survey of 288 U.S. and U.K. agency professionals, reported that 62% of U.S. agencies planned to include YouTube in CTV buys.[7] The sample is not a census of the market, but it does show why this is no longer a niche platform adjustment. More teams are already moving YouTube into the CTV budget conversation; genre plans make the planning assumptions more granular.

The Q3-Q4 2026 Planning Standard

A workable YouTube TV genre-plan strategy does not need to overcomplicate every buy. It does need to stop pretending that one platform label guarantees one audience pool. The planning standard for the second half of 2026 should be straightforward: use genre inventory when the audience, context, or creative depends on it; use broader coverage when the campaign needs household reach; and report frequency in a way that shows where delivery actually landed.

- Before the campaign launches, rebuild reach curves with Base, Sports, Entertainment, News, and relevant niche tiers treated as distinct inventory assumptions.

- During flight, monitor whether spend is concentrating in one genre plan faster than the campaign objective can justify.

- After flight, evaluate completed reach, effective frequency, brand lift, and incrementality by context rather than relying only on aggregate YouTube TV delivery.

- For sports-heavy Q4 plans, keep ESPN Unlimited as a fall-2026 scenario until access and inventory availability are confirmed.

The genre plans make YouTube TV more targetable, but only for teams that do the planning maintenance. Subscriber self-selection can reduce waste, sharpen context, and make CTV budget easier to defend. If the reach model still assumes one homogeneous YouTube TV audience, migration will show up later as uneven frequency, narrower exposure, and a plan that looked efficient only because it was averaged too broadly.

References

- YouTube TV Reveals Pricing, Channels for Lower-Cost Packages — Variety, Feb. 9, 2026

- Introducing YouTube TV plans launching early 2026 — YouTube Blog

- What Advertisers Need to Know About YouTube in 2026 — Tatari

- YouTube: Rising prices, shifting balance of CTV in 2026 — eMarketer

- YouTube Statistics 2026: 180+ Platform Data Points — Digital Applied

- How YouTube TV Advertising Works — AI Digital

- YouTube Nears TV Ad 'Tipping Point' — Business Insider, Jan. 2026

Comments

Join the discussion with an anonymous comment.