Acorns and Fidelity Go

A head-to-head comparison of Acorns and Fidelity Go robo-advisors, breaking down the balance-dependent pricing crossover and behavioral features that determine which platform costs less and fits your investing style.

Marketing Categories

⚠ Notable Limitations

No tax-loss harvesting (Acorns); no spare-change features (Fidelity Go)

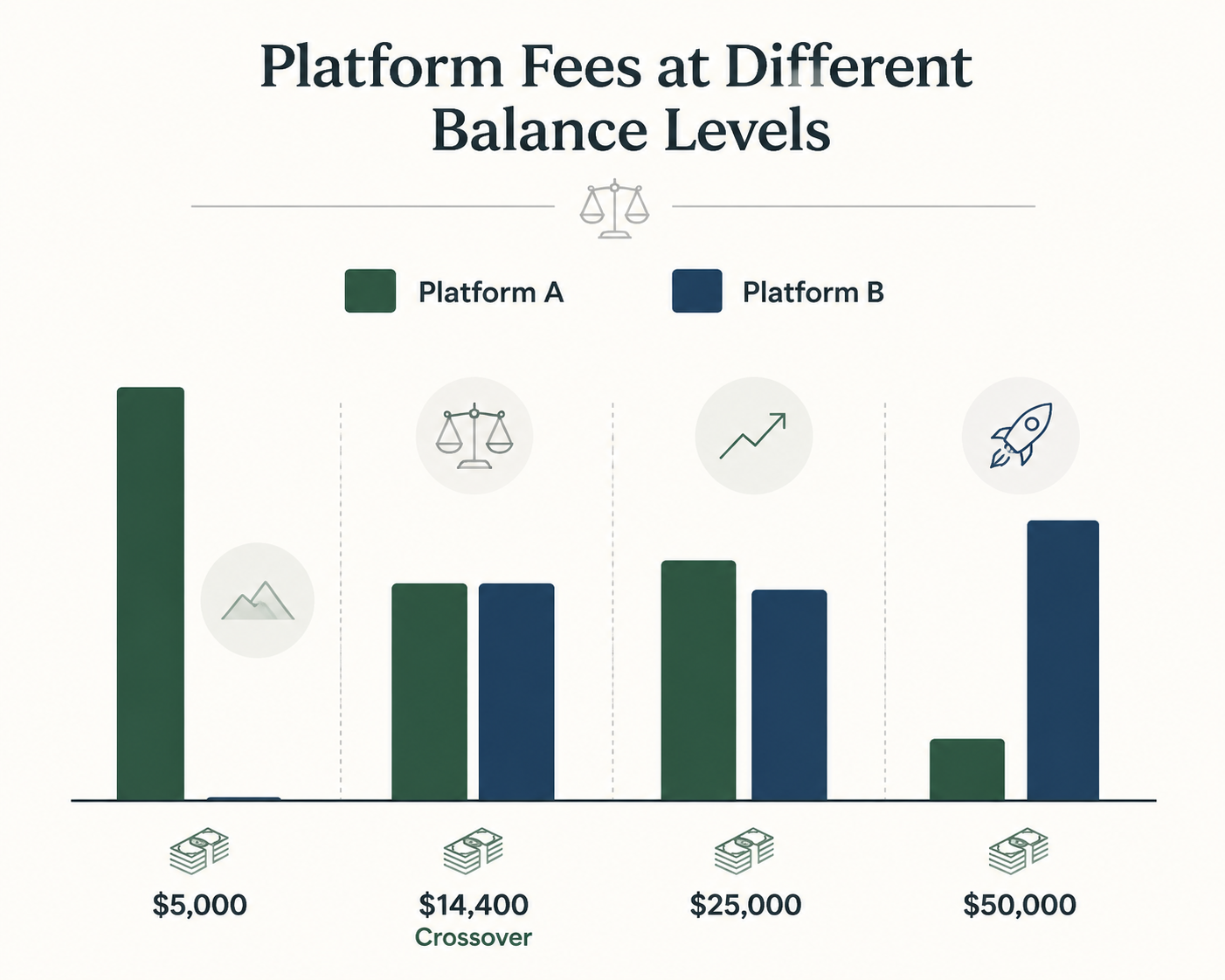

If the question is simply which robo-advisor is cheaper, the first answer is this: Fidelity Go is cheaper for low balances because it charges a $0 advisory fee below $25,000, while Acorns Bronze costs $3 per month, or $36 per year. Once Fidelity Go’s 0.35% advisory fee applies, Acorns’ flat Bronze subscription becomes cheaper at roughly a $14,400 balance. That crossover is a pricing guide, not the whole decision, because Fidelity Go’s real fee schedule stays free under $25,000 while Acorns charges even on a very small account.[1][2]

That is the receipt-on-the-table version of the Acorns vs. Fidelity Go comparison. At $5,000, Acorns Bronze costs $36 per year, which works out to 0.72% of the account, while Fidelity Go costs $0. At $50,000, Fidelity Go’s 0.35% fee would be $175 per year, while Acorns Bronze is still $36 per year. The awkward middle is where people often misread the comparison: the $14,400 figure is a rough flat-fee-versus-AUM guide, while Fidelity Go’s actual $0-under-$25,000 policy still matters more for anyone below that threshold.[1][2][3]

The Pricing Math Before the Preference Talk

Acorns and Fidelity Go use different pricing shapes. Acorns Bronze is a flat subscription. Fidelity Go is free up to a point, then percentage-based. That makes any blanket claim like “Acorns is cheaper” or “Fidelity is cheaper” too loose to be useful.

| Balance | Acorns Bronze | Fidelity Go | Cheaper on explicit advisory/platform fee |

|---|---|---|---|

| $5,000 | $36/year, about 0.72% effective cost | $0 advisory fee | Fidelity Go |

| $14,400 | About $36/year | Rough AUM-fee crossover against a 0.35% model | Pricing guide only; Fidelity Go is still free below $25,000 |

| $25,000 | $36/year | 0.35% fee begins above the free tier | Depends on exact fee application and tier, but Acorns becomes more favorable once Fidelity’s AUM fee applies |

| $50,000 | $36/year | $175/year at 0.35% | Acorns Bronze |

The table uses Acorns Bronze’s $36 annual subscription and Fidelity Go’s $0 advisory fee below $25,000 and 0.35% annual advisory fee above $25,000.[1][2] The $50,000 example is the cleanest high-balance comparison: 0.35% of $50,000 is $175, so Acorns Bronze costs far less if the only variable is the platform fee.[1][2]

The small-balance case is where the flat subscription deserves more suspicion. A $3 monthly fee sounds harmless because it is priced like a coffee add-on, not like an investment expense. On a $5,000 balance, though, $36 per year is 0.72% before considering fund costs or any other financial trade-off. Fidelity Go’s listed advisory fee at that balance is $0, and its managed portfolios use Fidelity Flex funds with 0.00% expense ratios.[1]

That does not make Acorns irrational at $5,000. It means the user has to know what the $36 is buying. If it buys nothing more than a place to park money, the fee is expensive. If it buys the habit of actually investing every week because spare change and recurring transfers happen without another decision, the calculation is less tidy.

The $14,400 crossover is useful because it translates a flat subscription into the language of percentage fees. But Fidelity Go complicates the clean comparison by waiving its advisory fee below $25,000. So below $25,000, the practical answer remains: Fidelity Go is cheaper on explicit advisory/platform cost. Above the point where Fidelity’s 0.35% fee applies, Acorns Bronze can become meaningfully cheaper.

This Is an “AI Robo-Advisor” Comparison Only in the Loose Search-Term Sense

Neither Acorns nor Fidelity Go should be treated as a modern generative-AI portfolio manager. In practical terms, these are automated investing services: the user answers questions, the platform assigns or recommends a portfolio, contributions are invested according to that model, and the account is rebalanced by rules. Calling that “AI” is common search language, but it can make the product sound more adaptive or predictive than the materials support.

That clarification matters because it keeps the comparison grounded. The decision is not whether Acorns or Fidelity Go has the smarter investing brain. The decision is whether the pricing model, account features, and automation style solve the problem the investor actually has.

Where Acorns Earns Its Fee

Acorns is easier to understand if it is judged less like a stripped-down brokerage account and more like a behavior system. Its signature feature is Round-Ups: purchases can be rounded up and the difference invested. Acorns says more than $4 billion has been invested through Round-Ups to date.[2]

That number does not prove Round-Ups outperform another investing approach. It does show that the feature is not decorative. It is the product’s central argument: many people do not need another dashboard as much as they need money to move before they have time to talk themselves out of it.

For someone who already transfers a fixed amount into investments every payday, Round-Ups may be unnecessary. For someone who has meant to start for two years, it can be the difference between a plan and an account that actually receives money. That is why a small account can rationally pay a subscription even when the effective percentage looks high. The fee is buying automation that reaches into daily spending, not just portfolio management.

Acorns also has features that push it toward household and long-term habit formation. Its materials describe kids’ investing accounts and an IRA match of up to 3% on the Gold tier, which costs $72 per year.[2] Those features belong in the decision only if the user will actually use them. Paying for a richer tier because an IRA match sounds good, then failing to contribute enough for the match to matter, is just a more respectable-looking version of wasting money.

The weak spot is that Acorns does not offer every feature a more conventional managed-account shopper may expect. The available sources identify no tax-loss harvesting and no human advisor access for Acorns.[2] For a taxable account at a larger balance, or for someone who wants a human to talk through choices, that absence may matter more than the low flat Bronze price.

Where Fidelity Go Is the Cleaner Starter Choice

Fidelity Go is the cleaner answer for a beginner who wants managed investing without a subscription nibbling at a small balance. It has a $0 minimum, a $0 advisory fee below $25,000, and uses Fidelity Flex funds with 0.00% expense ratios.[1] That combination is hard to beat for someone starting from a few hundred or a few thousand dollars and trying to avoid fee drag.

It also sits inside a more conventional investing relationship. At $25,000 and above, Fidelity Go includes access to human financial coaches, and the available sources identify tax-loss harvesting at that same threshold.[1] Those features fit a person who wants managed investing but still wants the comfort of a large brokerage environment and a human support option once the account grows.

The trade-off is that Fidelity Go does not have Acorns’ spare-change machinery. The available sources identify no Round-Ups, no IRA match, and no kids’ accounts for Fidelity Go.[1] If the user needs a product that turns everyday transactions into investing prompts, Fidelity Go is not built around that behavior.

That is not a defect for everyone. Some people do better with a plain recurring transfer and fewer gamified cues. A professional who wants to set a monthly contribution, avoid a subscription, and keep investing under the Fidelity umbrella has a straightforward reason to choose Fidelity Go. The platform’s advantage is not that it feels more exciting. It is that the fee schedule stays quiet while the account is small.

The Behavioral Fit Can Overrule the Cheapest Line Item

There are two common mistakes in this comparison. The first is ignoring effective cost: $36 per year is not the same thing on a $500 account as it is on a $50,000 account. The second is pretending the cheapest tool is best even if the person will not fund it.

For a tired, late-starting investor, inertia is not a minor inconvenience. It is the opponent. Acorns attacks that problem by making small investments happen in the background. Fidelity Go attacks a different problem: giving a cost-conscious beginner a managed portfolio without requiring a minimum balance or charging an advisory fee before $25,000.

This is also where using both can make sense, as long as the overlap is intentional. An investor might use Acorns for Round-Ups and habit-building while keeping broader managed or self-directed investing at Fidelity. That is not a magic optimization strategy. It is a way to separate two jobs: automatic accumulation on one side, broader investment management on the other.

The danger in a dual setup is fee clutter. A small Acorns subscription, a managed Fidelity account, and unused premium features can quietly become a pile of “almost nothing” charges and half-used accounts. If the investor cannot explain why each account exists, the simpler setup is probably better.

Performance Should Not Decide This Comparison

Trailing performance data through year-end 2024 is not a strong basis for choosing between these two services. It can describe what happened in past portfolios over a past window, but it does not tell a new investor which service will perform better next. For this comparison, fee structure and behavior fit carry more weight than return tables.

That may feel unsatisfying because performance sounds like the clean scoreboard. But with automated diversified portfolios, the user’s funding behavior, tax situation, account size, and fees can easily matter more than a backward-looking ranking. The best robo-advisor on paper is not very useful if it sits unfunded.

A Practical Decision Rule

- Choose Fidelity Go if your balance is below $25,000 and your main goal is the lowest explicit advisory/platform cost.

- Choose Fidelity Go if you want a $0 minimum, Fidelity Flex funds with 0.00% expense ratios, and access to human financial coaches once the account reaches the stated threshold.[1]

- Consider Acorns Bronze if your balance is high enough that a flat $36 annual subscription compares favorably with a 0.35% AUM fee.

- Consider Acorns if Round-Ups, passive accumulation, kids’ accounts, or the Gold tier IRA match are features you will actually use.[2]

- Avoid paying for either platform feature set if the account will sit unfunded or the paid features are mostly aspirational.

So, which robo-advisor is cheaper — Acorns or Fidelity Go? For a low-balance investor looking only at explicit fees, Fidelity Go wins. For a larger balance where Fidelity Go’s 0.35% fee applies, Acorns Bronze can be cheaper, with the $14,400 crossover serving as the rough math guide and the $25,000 Fidelity free-fee threshold serving as the real-world checkpoint.

The better fit is the one that matches how money will actually move. If you will fund an account consistently without nudges, Fidelity Go’s low-friction pricing is compelling. If Round-Ups and passive saving features are what make investing happen at all, Acorns can justify a fee that looks expensive on a small spreadsheet. Pricing and features in this comparison reflect mid-2026 materials; subscription tiers, fee thresholds, fund details, and promotional offers can change.

References

- Fidelity Go Overview — Fidelity

- Acorns vs. Fidelity: How They Compare (2026) — Acorns

- Acorns vs. Betterment & Wealthfront in 2026 — Acorns

Comments

Join the discussion with an anonymous comment.